Sustainable management is no longer a buzzword; rather, global challenges, legal requirements and competitive factors are forcing companies to operate sustainably. In this article, you will find out exactly what is involved and what options you have to tread the path to sustainable management.

Definition of Sustainability

Sustainable thinking is already attributed to Hans Carl von Carlowitz, who is said to have recommended in 1713: “Cut only as much wood as the forest can handle.” Thus, von Carlowitz translated a resource-conserving approach to thinking into a principle for action.

Sustainability is defined as a state in which the needs of the present generation are met without limiting the possibilities of future generations.

This means that sustainability is not an “extra issue”; rather, it is a cross-cutting issue that should always be considered everywhere. Sustainability affects all areas of the economy and should be integrated into corporate strategy and operational processes.

Global Challenges

A wide range of global challenges demand sustainable business practices. These global challenges include, above all:

- the global shortage of raw materials

- climate change with its ecological, social and economic consequences

- political upheavals

- the rise in energy prices

- inflation with associated price and wage increases

- supply chain bottlenecks caused directly by global networking

- market concentrations

- increasing transparency due to digital networking

- requirements for integration into a circular economy

- the increasing shortage of skilled workers

- the changing values in our societies

- the decreasing willingness of insurers to assume claims risks

These global challenges suggest sustainable business practices to companies.

Legal Basis

Legal requirements also increasingly demand sustainable management.

Corporate Sustainability Reporting Directive (CSRD)

The European Union wants to be a climate-neutral continent by 2050. To this end, it has issued the EU Corporate Sustainable Reporting Directive (CSRD), which is to be implemented in national legislation. According to this directive, companies are to prepare annual qualitative and non-financial sustainability reports. Transparency is intended to make greenwashing more difficult for companies.

Corporate Social Responsibility-Directive Implementation Law (CSR-RUG)

The Corporate Social Responsibility Directive Implementation Law (CSR-RUG) is the German interpretation of this European directive. The law requires companies to make non-financial reports. The reporting obligation initially applies to large companies, but will gradually include smaller companies as well.

2023: Companies with > 500 employees, 40 MEUR sales and 20 MEUR balance sheet total

2024: Companies with > 250 employees, 40 MEUR sales and 20 MEUR balance sheet total

2026: In addition, all listed small and medium-sized enterprises (SMEs).

Other countries are implementing similar laws.

Environmental Product Declaration (EPD)

This EU directive on environmental product declaration based on the ISO 14040/44 life cycle assessment and the ISO 14025 standard, which provides principles and procedures for Type III environmental labels. In the construction industry, the EN 15804 standard is also used, which relates to building products.

The EPD Directive requires companies to provide a declaration covering the entire product life cycle, i.e. from the extraction of raw materials, through product manufacture and product use, to the disposal of the products produced. The Environmental Product Declaration allows an objective assessment of product sustainability. An EPD is created through the steps of preparation, verification by a neutral body, subsequent completion and publication.

Supply Chain Due Diligence Act

There is much human misery in the world caused by the economic exploitation of people. In order to prevent this deplorable state of affairs in the future and to create legal certainty for affected people and German companies, the Supply Chain Due Diligence Act (Lieferkettensorgfaltspflichtengesetz – LkSG) was introduced in 2023, which requires companies to comply with basic human rights standards. The LkSG imposes a reporting obligation on companies regarding human rights and environmental risks in the supply chain. It establishes responsibility for the entire supply chain. Compliance with the LkSG is monitored by the Federal Office of Economics and Export Control (BAFA). Reports submitted are reviewed; complaints received are followed up.

The LkSG may put German companies at a disadvantage in international competition, but it helps protect human rights.

Other countries may implement similar acts.

Global Reporting Initiative (GRI)

To this end, the Global Reporting Initiative (GRI) has introduced comprehensive global standards for the preparation of sustainability reports. The GRI was founded in 1997 by CERES (Coalition of Environmentally Responsible Economies) in cooperation with the United Nations Environment Programme.

The aim of the GRI is to help governments, companies, investors, employees and the public to standardize, make transparent and compare sustainability reports. To this end, the GRI recommends the use of certain metrics and performance indicators in sustainability reports. In its 2016 version, the GRI guideline includes 86 indicators, namely:

- 11 economic performance indicators,

- 35 environmental performance indicators

- and 40 societal or social performance indicators.

Since 01.07.2018, compliance with the GRI guideline for the preparation of sustainability reports has been mandatory for all companies. In order to better meet industry specifics, the GRI has also created so-called Sector Guides, which are included.

The GRI recommendations for reporting on greenhouse gas emissions are based on the GHG Protocol of the World Resources Institute and the World Business Council for Sustainable Development.

Financial institutions now expect their borrowing companies to produce sustainability reports that include these GRI-recommended metrics and performance indicators.

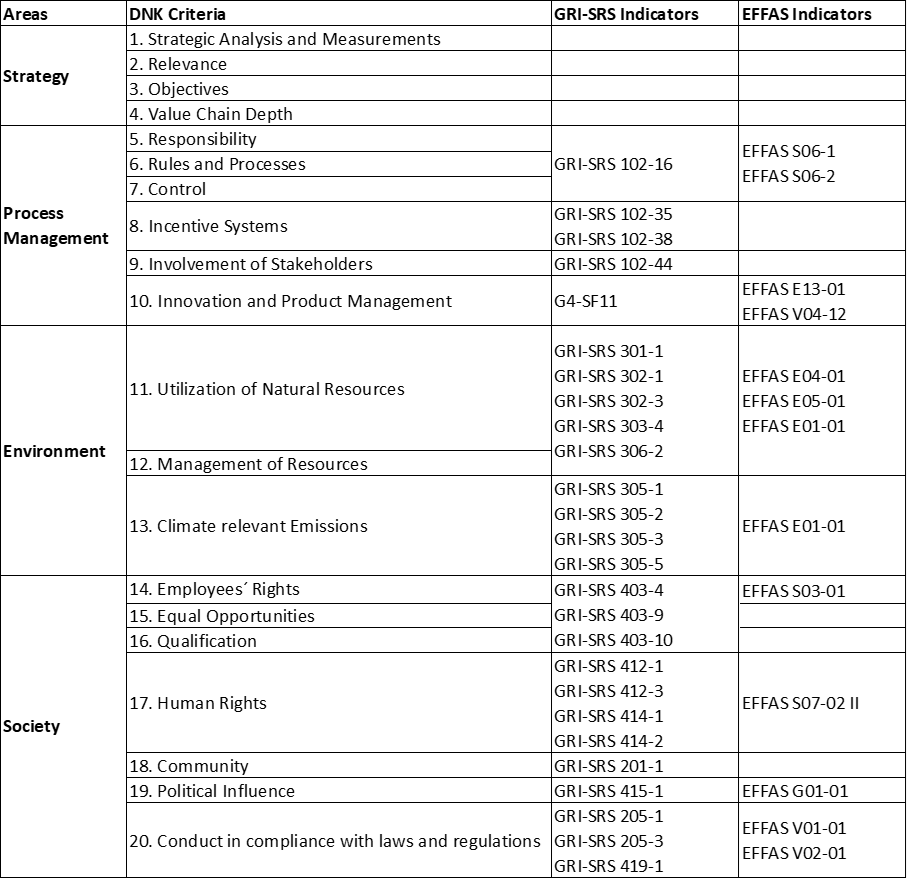

German Sustainability Codex – Deutscher Nachhaltigkeitskodex (DNK)

Several countries have launched national sustainability codice.

The German Sustainability Codex (DNK) was derived in Germany from 16 criteria of the European Federation of Financial Analysts Societies (EFFAS) and the 28 performance indicators of the GRI (GRI-SRS) and has been introduced as binding for larger German companies. A guideline is currently (2023) being developed for SMEs. Reports in accordance with the German Sustainability Codex (DNK) serve as a strategic inventory of sustainability. Compared with the RGI guideline, however, the German Sustainability Codex (DNK) is a less comprehensive guideline.

The German Sustainability Codex (DNK) is structured in four blocks:

- Strategy

- Process management

- Environment

- Society

Comparison of the DNK criteria with the GRI-SRS indicators and the EFFAS indicators:

The Codex provides for working according to both the “comply” principle and the “explain” principle. The comply principle requires companies to prepare a report on the basis of data and facts on the issues under scrutiny, while the explain principle calls for gaps to be openly identified.

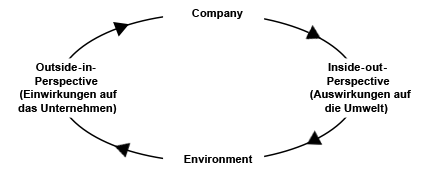

A special feature of the Sustainability Codex report is the requirement to perform what is known as double materiality. This is understood to mean the influences from the outside-in perspective and the influences from the inside-out perspective. From the outside-in perspective, the main opportunities and risks that arise for the company as a result of sustainable management are to be taken up. From the inside-out perspective, the main positive and negative effects of sustainable management on society and the environment should be recorded. Going through this exercise for your own company can reveal interesting insights. The interactions between the outside-in perspective and the inside-out perspective can best be illustrated in a cycle.

Arguments for Sustainable Management

There are good reasons for companies to do business sustainably:

- Reduce the footprint.

By definition, sustainable businesses reduce their environmental footprint. They leave behind less waste and emit fewer harmful exhaust gases and wastewater into the environment. In this way, they contribute to environmental protection.

- Meeting legal requirements

The EU wants to become completely climate-neutral by 2050. The German government has set itself the goal of reducing net greenhouse gas emissions by 55% by 2030 compared with 1990 levels. To this end, legal requirements have been passed, in particular the Corporate Social Responsibility Directive Implementation Act (CSR-RUG). More and more companies must meet the legal requirements for their corporate social responsibility (SCR).

- Secure orders

More and more companies must comply with the requirements of the Corporate Social Responsibility Directive Implementation Act (CRS-RUG). To do so, they are required to include their suppliers in the reporting obligation. Suppliers who do not (or cannot) comply with this reporting obligation may not be considered for the award of contracts.

As a rule, participation in tenders for public sector contracts is hardly possible in Germany without proof of sustainable management. Other countries are following suit.

- Reducing costs

Sustainable management may initially be associated with cost increases, but sustainable management can actually save costs. The conscious selection of raw materials, the deliberate choice of manufacturing processes, process optimization, appropriate measures to reduce energy consumption and supply chain security are such levers for cost reduction. The separability and recyclability of materials can increase the value of discarded products. Companies can profit from this. The commitment to the proven longevity of products and the reusability of discarded products in other areas of application can support sales prices in a competitive comparison. It therefore makes sense to identify the corresponding potential.

- Attracting and retaining employees

Employees are increasingly demanding CSR-compliant behavior from their employers. The interest of employees is not limited to the ecological aspects of sustainability, but also includes social aspects. Employees want to find meaning in their work. They are also interested in flexitime and work models that are in line with life phases. They also observe how employers deal with the issue of inclusion.

- Strengthening and maintaining the image

Companies that do good and regularly report on it in PR measures can specifically strengthen and maintain their image. This gives them a more positive image in the public debate and more favorable conditions for being included in value creation networks. Recognized and established quality labels such as “Fairtrade” or “Fairstone” are suitable for this purpose.

- Obtaining new credits

Proof of sustainable management is becoming an important criterion for companies when it comes to credit rating by credit institutions. A sustainability report can help improve credit ratings and make it easier to access new loans and negotiate more favorable loan terms.

- Securing succession

In the search for entrepreneurial successors or institutional prospective buyers in the course of succession planning, sustainably operating companies can demonstrate their future viability better than non-sustainably operating companies. As a rule, this has an impact on the achievable purchase price.

Navigator for Sustainable Management

More and more companies, even smaller ones, are being required to submit a sustainability report, either by their customers or as a result of increasingly stringent legal requirements. Preparing a sustainability report is a demanding task. In addition to the formalities that have to be taken into account, a lot of data has to be collected within the company. This is time-consuming. Not every company is prepared for this. There are specialized management consultants who support companies in the preparation of their sustainability report.

The Sustainability and Internationalization section of the Zentralstelle für die Weiterbildung im Handwerk e. V. (ZWH) has created a useful implementation aid in the form of its Navigator.

The Navigator guides through the creation of the sustainability report in seven steps:

- value chain (as the basis for the business).

- exchange with stakeholders

- consumption and management of natural resources

- working conditions, health protection and qualification of employees

- social and political commitment

- sustainability goals

- action plan

With this approach, ZWH clearly demonstrates that sustainability is not a state, but a process. Those who perceive sustainability as a process can better develop their company in terms of sustainable management.

Summary

Global challenges and legal requirements call for sustainable business practices. Legal requirements include compliance with the Corporate Sustainability Reporting Directive (CSRD), which is being transposed into national legislation. The laws initially relate to application at large companies, but will gradually be extended to application at smaller companies as well. First and foremost, they deal with reporting requirements on sustainable business practices.

In addition to these constraints, however, there are a number of good reasons for companies to switch to sustainable business practices, including contributing to environmental protection and human rights-compliant business practices. Furthermore, companies that operate sustainably can gain advantages in terms of sales and costs, better secure supply chains, and attract and retain a better workforce.

Specialized management consultants are available for planning and implementing processes that describe the path to sustainable management. The Zentralstelle für Weiterbildung im Handwerk (ZWK) offers a useful tool with its Navigator.